Driven by rapidly maturing underlying technologies and increasing regulatory clarity, the drone industry is at the tipping point of unlocking Beyond Visual Line of Sight (BVLOS) operations and, with it, a large untapped market for drone and drone-transported cargo insurance. Within the BVLOS ecosystem, drone management platforms fulfill the most critical role of flight-path risk management and automated approval.

Unlocking the promise of commercial drone flights

Drones have long been promised as a potential way to move people and goods more efficiently. The industry saw substantial early excitement and investment but has largely underperformed expectations over the past decade, with e-commerce packages still being delivered by UPS drivers and people still traveling aboard aircraft flown by human pilots. Despite slow early adoption, the drone industry has advanced substantially, with BVLOS technology and hardware components nearing commercial readiness and the regulatory requirements for deployment becoming increasingly solidified. As a result of these developments, we are now at the cusp of enabling BVLOS flights, which is the key to unlocking the promise and commercial productivity of drones.

Over the past decade, the core technologies underpinning drones (batteries, control software, and communications) have progressed substantially. As a result, quality – measured in flight duration and the capability of operating in challenging conditions – has improved, while component costs have declined. For example, the very first DJI drone (Phantom 1) could fly for only 10 minutes on a full charge in ideal sunny weather conditions, while the company’s most recent model (M300 RTK) can operate in heavy rain, high wind, and icy conditions down to -20° C for nearly an hour. Similarly, substantial progress has been made within the large-form-factor drone transport platforms, with several companies, such as Joby Aviation, expecting to receive their Aircraft Type Certifications (required to operate commercial flights) by next year.

Concurrent with the development of core drone technologies has been the increasing regulatory clarity offered by the Federal Aviation Administration (FAA), which manages all U.S. airspace. Such clarity around how drones are permitted to operate is critical for commercialization, as clear regulations provide the framework necessary for drone operators to architect for scaled deployments. Two of the most essential components, Remote ID and Unmanned Aircraft System Traffic Management (UTM), were solidified in 2021:

- Remote ID – Remote ID mandates that every drone must broadcast in real-time its unique signature. Similar to automotive vehicle registrations, these IDs can be used by government agencies to understand the various parties operating in the airspace and represent a critical step in enabling safety. Enforcement of Remote ID will begin in September 2023 and will be managed by local and state governments.

- UTM – Like its current program for managing Visual Line of Sight (VLOS) drone flights (Low Altitude Authorization and Notification Capability, or LAANC), the FAA intends to leverage approved third-party platforms to manage commercial BVLOS drone flights. This framework, known as UTM, will require such drone management platforms to integrate vast amounts of data streams in real-time and across various stakeholders to de-conflict airspace and ensure operating safety.

The ability to operate BVLOS represents the most critical piece in unlocking commercial drone flight volume and revenue, as the industry is currently limited by the significant logistical challenge of needing to maintain a visual line of sight with drones during operations. Such challenges can be seen prominently within the parcel-delivery space. Amazon alone delivered more than 4.2B packages in 2020, with USPS, UPS, and FedEx combining for an additional 15.8B packages. In the current VLOS requirement model for drone deliveries, all 20B packages would need to be monitored manually and individually, creating an unprofitable and untenable proposition for logistics providers.

Drone management platforms and the operationalization of BVLOS

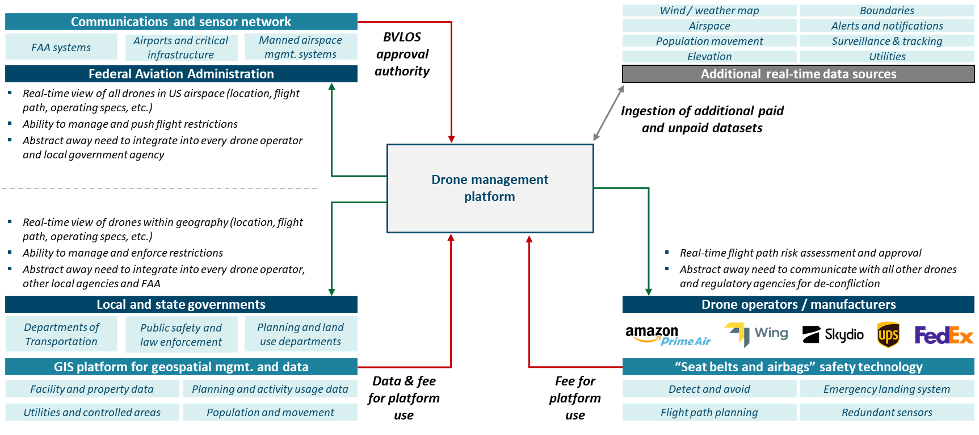

The combination of maturing technologies and regulatory clarity is beginning to enable the safe operations of drones beyond the visual line of sight. In order to fly BVLOS, drone operators must complete a two-step process with the FAA. Operators will be required to secure Type Certification for their use case by demonstrating their drone’s safety case to the FAA. This includes the ability to detect and avoid obstacles and safely land in emergency scenarios, among other safety features. With underlying drone technology rapidly maturing, several drone operators, such as Matternet (operated by UPS), have achieved Type Certification.

Once the drone becomes certified, the operator must obtain approval for individual flights through the FAA’s UTM system. At the core of this system are drone management platforms:

Drone management platforms provide a unified view of risk and safety to all stakeholders by integrating across the drone ecosystem, from the FAA to local government agencies to drone operators. By leveraging these integrations and additional real-time datasets, platforms such as these can generate a risk assessment and score of every drone flight, adjusted dynamically based on air and ground risk factors. Most importantly, real-time BVLOS flight approvals are granted in real-time by these platforms, based on operating criteria and risk scores.

What does this mean for insurance?

As BVLOS begins to unlock the promise of commercial flights at scale, drones will become an increasingly integral component of the logistics ecosystem. In fact, of the 20B parcels delivered in 2020, an estimated 12.9B could be delivered by drones based on package size, geography, and other factors. This, in turn, will also create a rapidly growing opportunity for commercial carriers to insure drones. While premiums for BVLOS drone insurance will ultimately be refined over time, even at today’s drone insurance rates of approximately $500 per drone per year, BVLOS drone insurance for package delivery alone represents a $160B+ market opportunity.

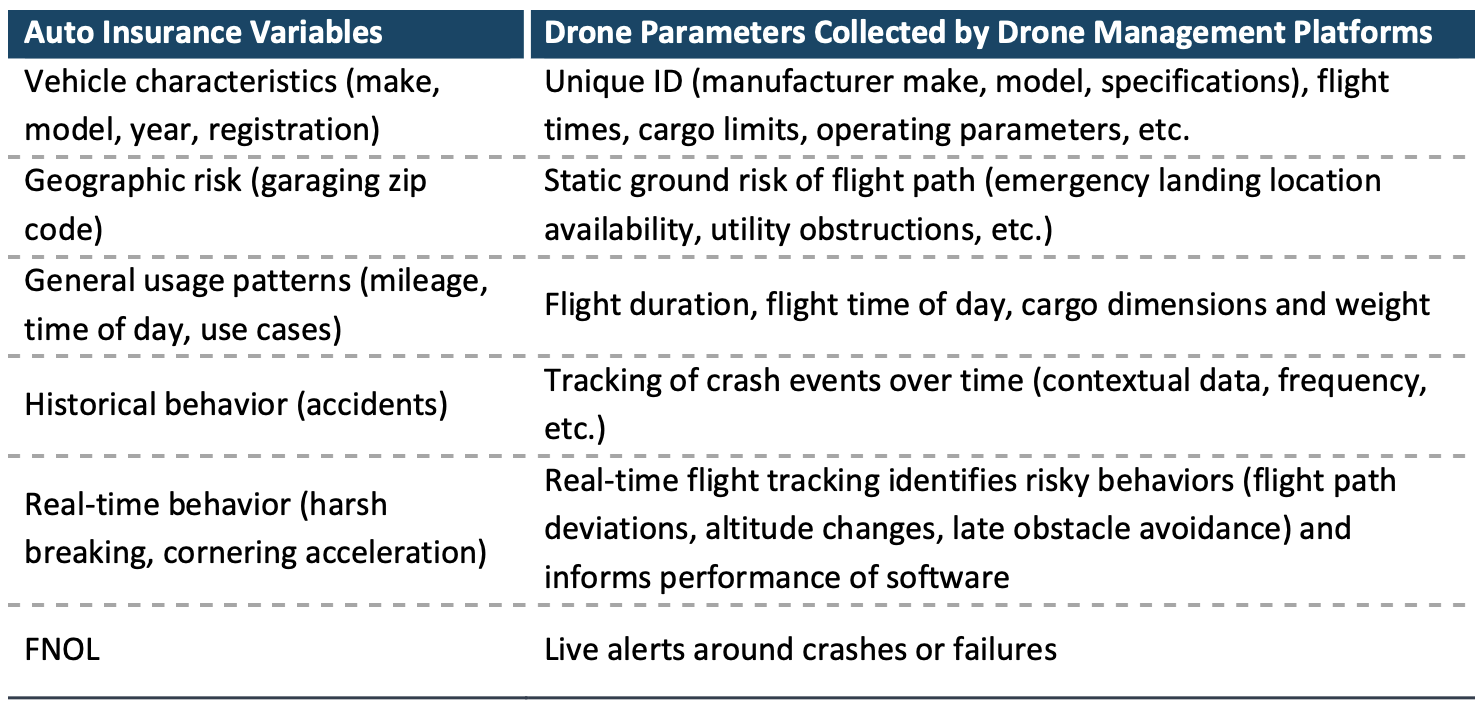

As insurers evaluate and look to enter this market as part of a broader commercial logistics insurance offering, a partnership with a drone management platform could enable access to datasets relevant for risk underwriting and management. While new factors and correlations will undoubtedly be discovered, there are significant overlaps today between current auto insurance variables and the analogous drone parameters collected by drone management platforms for flight-path risk calculations:

Furthermore, drone management platforms could represent a unique leveraged distribution channel for insurance products. As such platforms will be required to procure approvals for any commercial BVLOS operations, a partnership could ultimately allow insurers to offer and potentially embed insurance products for drone operators at the customer’s point of need.