Following the rise of direct-to-consumer models in personal auto and home insurance, many expected commercial insurance independent agents (IAs) would similarly be displaced by direct-to-policyholder technologies.

Online channel disintermediation is endemic across all industries. However, commercial lines IAs would tell you the opposite is occurring. The complexity of commercial lines insurance products and their underlying application, service, and claims processes continue to cement the customer value proposition offered by IAs. However, commercial lines IAs still face technology-driven challenges and opportunities. The antiquated technology stacks that most IAs use seriously restrict their ability to grow and improve profitability. This technology deficit cracks open the door for direct-to-policyholder competitors to make inroads into specific market segments.

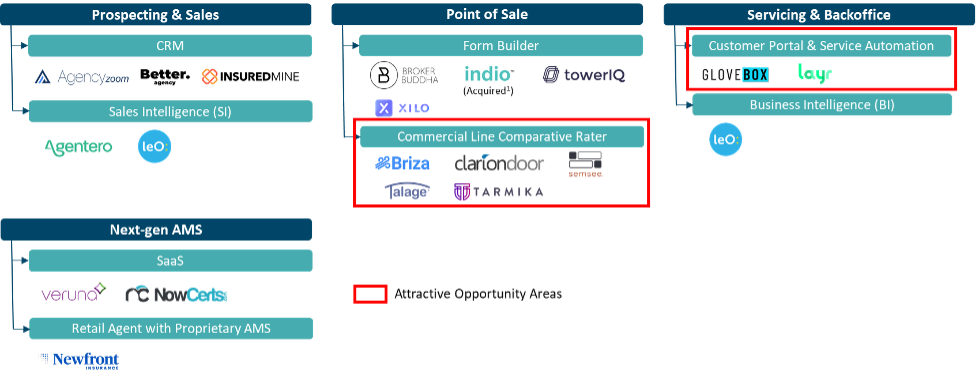

In response, a burgeoning ecosystem of new technologies and innovations has formed to enable IAs to work more effectively. Two up-and-coming technologies empowering IAs are commercial lines comparative raters and servicing automation.

Commercial insurance IA channel market dynamics

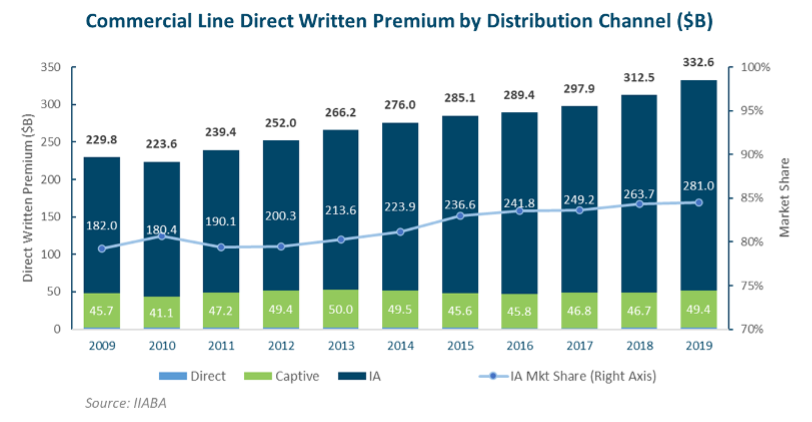

IAs sell insurance policies offered by multiple insurance carriers, while captive agents can only sell products of the carrier for whom they work. The ability to offer a greater variety of products gives IAs a distinct advantage in the commercial market, mainly because of the heterogeneous needs of commercial clients. As a result, IAs control a majority of the distribution for commercial lines insurance.

In contrast to personal lines, commercial lines IAs’ market share has been steadily going up, reaching 84.5% in 2019.

Commercial lines policies, in general, are more complicated than personal lines policies. For instance, IAs typically review only the declaration pages of personal lines policies, but they often review the entire document for commercial lines policies, which are usually more than 100 pages. Given the larger premium and coverage amounts of a commercial lines policy, many moving parts must be considered throughout the application process. As a result, commercial customers need the handholding offered by IAs.

Additionally, the commercial lines insurance market is more fragmented. The collective market share of the top 10 commercial lines carriers stood at 31.2% in 2020, while this number was 58.9% for personal auto and 43.5% for home. Each carrier has its own nuanced risk appetite, such as types of risk, geography quotas, and even the line of insurance offered (e.g., workers’ comp vs. general liability, etc.). Most commercial lines policies are a combination of multiple insurance lines. Thus, IAs offer customers value with customized analysis, consultation, and market access to the most appropriate carriers.

Finally, application forms of commercial lines insurance vary significantly from carrier to carrier, making self-service less approachable than personal lines insurance where applications are increasingly standardized and simplified. These factors enable IAs to offer a stronger value proposition to their commercial lines clients.

Antiquated IA technology creates opportunities for disruption, especially in small commercial

IAs use carriers’ agent portals and email to quote and bind and use an Agency Management System (AMS) for the rest of their workflows, including everything from CRM to servicing and bookkeeping. These tools were built years or even decades ago, without modern architecture or APIs. Systems are siloed from each other and often require a lot of repetitive data entry. Vertafore and Applied Systems constitute a duopoly in the AMS market, collectively controlling more than 85% of the market. Together, they generate more than $1B in subscription revenue each year. Their software solutions have only recently started to migrate from on-premises to cloud-based architectures. They are slow to develop new products internally and are heavily dependent on acquisitions for innovation. The result is a fragmented technology platform for both companies, leading to an inferior user experience.

The small commercial market is where new technologies would be the most helpful to IAs. Small accounts generate lower commissions for IAs per policy. However, the time required to shop applications across carriers and service policyholders doesn’t decrease proportionally, making them much less profitable than larger accounts. IAs have strong incentives to deploy new technologies to improve efficiency and profitability for their small commercial books.

Emerging IA enablement tech ecosystem

These challenges, however, have given rise to a growing ecosystem of technologies and innovations to enable IAs to increase productivity and save costs. Startups are creating innovative solutions to modernize IAs’ entire workflow, ranging from prospecting to point-of-sale to servicing.

Historically, AMS providers employed a subscription business model. New players are offering disruptive business models, either charging a percentage share of the total agency commission or generating revenue from carriers, drastically increasing the total addressable market of IA enablement tech companies. These new business models are supported by better user experiences and compelling ROIs offered by these new technology solutions. For example, IAs can quickly evaluate the ROI on a new solution by calculating the number of hours they would save on quoting and servicing. An aging agent population, coupled with the pandemic labor shortage, has made these new technologies even more compelling to IAs.

Repetitive data entry is the №1 pain point for commercial lines IAs

Point-of-sale for IAs involves quoting and binding. Quoting is the №1 pain point for IAs. IAs currently need to submit to each carrier either through each carrier’s unique agent portal or via email. Each carrier also has its own supplementary forms to be filled out, meaning that IAs cannot submit one form to all carriers. It takes about 15 minutes for data entry per carrier submission, amounting to hours for IAs to complete quoting for one customer. A large amount of time is spent on repetitive data entry. To save time, experienced brokers will guess where the carrier appetites are and only quote from three to four carriers — making the process far from ideal.

Several companies, such as Talage and Semsee, are building commercial lines comparative raters. The raters compile multiple applications into one data entry and remove the guesswork. Some commercial lines carriers have ramped up their API infrastructure in the last few years, providing a minimum viable comparison foundation for these modern raters. However, many commercial lines carriers are still early in their API development. In addition to rater technology, IA enablement software providers try to differentiate their solutions by offering unique value-add products and features. Talage, for example, offers Wheelhouse, an out-of-the-box digital storefront tool, to enable IAs to set up their online presence easily.

The current servicing model is not sustainable for small commercial accounts

Servicing is another major cost center for IAs, especially for small commercial accounts, which generate a much lower commission per policy than larger accounts. If an IA spends more than a few hours each year on servicing a small commercial account, it becomes unprofitable.

Historically, very few companies worked on improving the servicing experience for IAs. But new startups are emerging to come to IAs’ rescue. For example, Layr leverages automation and its in-house account management team to allow IAs to outsource servicing for their entire books at variable cost (i.e., a percentage of the total commission). Such service makes it more economical for IAs to serve small commercial clients.

Innovative VC-funded IA enablement tech startups

Below are some examples of venture-funded innovators hoping to empower IAs.

What does this mean for the future?

Commercial lines insurance products are largely distributed through the IA channel and that will not change any time soon. While these enablement technologies benefit commercial lines insurance products the most, they can also improve processes for personal lines. For carriers, data and insights from these platforms could help guide future product development and can also help carriers better scale and manage their IA channels.

What are your thoughts on the future of commercial independent agents?